Other than the fact that we had an ice-covered tree rather than ice-covered statues, and of course no Christmas lights, this looks bizarrely similar to what happened to us a couple of weekends ago.

Ted, first report it to your insurance company, then give them time to compile a list of all the technicalities with which they’ll cut down on the amount of payment you’ll eventually see.

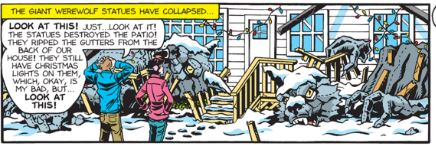

So the werewolf statues fell down and the artist gets a chance to try his hand in heavy line serial realism comic style. In ‘Sally Forth’. Are we honestly expected to care. At all. If so, why?

LikeLike

Really, they got off light. The gutters and some damage to the back porch. It’s not like the siding came off. But, yeah, the insurance isn’t gonna want to pay a dime.

LikeLike

Oh, those Forths!

At one time I did a little programming in Forth, enjoyed the well-written manual, and enjoyed the class that used it (not a course in programming per se, but in support of a topic).

And some people would refer to “running your deck” though that was not standard terminology.

LikeLike

The comments on Comics Kingdom are generally pretty brutal towards the strip, but lately it’s been really rough. Of course, they rightly point out that Ted and Sally can’t be too mad at the girls. After all, they could have had the statues removed months ago.

I did really enjoy the artwork in this strip, especially the big claw hand seeming to grasp the rail.

As far as insurance, I’m not even sure that would be covered. I mean, “My daughter and her friends attached large ramshackle statues to the house. After some months, they collapsed and damaged the house and deck. Give me money.” That might be a tough sell.

LikeLike

@Brian in STL: Unless Ted adds “If you *don’t* give us money, my daughter and her bandmates will come over to your office and sing one hundred and ninety-five choruses of each of their “Werewolves in Love” songlist to you.”

LikeLike

Well, based on my time as a residential claims adjuster and the policies I handled:

Damage caused by the falling werewolf statue would be covered up to the limit of the policy. Deductible applies.

If it were a neighbour’s statue and the neighbour was aware it was unstable (for example, if their had been complaints from Sally or evidence of it moving in high winds), we’d pay the claim and pursue the neighbour for damages.

If it were a tree and not a statue, there would be coverage but the extent of coverage would depend on the circumstances:

-tree fell and hit the structure and the tree was still resting on the structure, we would pay to remove the tree from the structure and the property. Damage to structure covered as per normal policy limits.

-tree fell and hit the structure, then fell off the structure and is resting on the ground, we pay for damage to the structure within normal policy limits. If it is a platinum policy we would also pay up to $5000 to remove the tree from the property. This does not include removal of stump or roots.

-tree fell and did not hit structure but is on ground creating a big damn mess. If you have a platinum policy, we’d pay up to $5000 to remove the tree from the property. This does not include removal of stump and/ or roots. A non-platinum policy, you’re on your own.

If the tree were not your tree but a neighbour’s tree, we would still pay whatever is appropriate based on the scenarios described above. We would NOT pursue neighbour for damages unless the tree was dead/dying and the neighbour knew this (due to an arborist’s report, city inspection, clearly visible evidence).

Now every jurisdiction and every insurance company is different, but what I have found is that complaints of us “ripping off” people and “looking for ways to not cover things” was me applying the policy as it was written and paying out according to that. The client, however, felt that I should pay out based on the imaginary policy that existed in their head. My advice is to read your home policy thoroughly. If you don’t understand some of the terminology call your insurer to ask for clarification. Your policy covers what it says it covers. It excludes what it says it excludes. Shop for your policy by coverage, not price.

I thought it was a hoot when people would argue with me about what their policy covered and how it was to be interpreted. I had read these policies literally hundreds of times. I was a go to guy in the department on policy knowledge. I challenged the audit people who failed me on a review of one of my cases because they were incorrect in their policy knowledge and won. So no, telling me it covers something it doesn’t isn’t going to fly. Not going to pay you what you’re not entitled to. That said, I hated my employer much more intensely than any customer possibly could and would gladly pay out for ANYTHING I could possibly justify paying out. I didn’t get to keep the money if I didn’t pay it out, after all. My policy knowledge meant I could find everything they were entitled to or that was questionable but that I could justify. All that said, my company was known to be permissive. I probably couldn’t have gotten away with the stuff I did at some other companies.

My experience is in Canada. I hear things work a bit differently in USA.

LikeLike

Singapore Bill: are you also secretly a superhero forced into hiding by the government?

LikeLike

@ larK: Shhhhh…

LikeLike

“are you also secretly a superhero forced into hiding by the government?”

according to the sequel, the supers are allowed to be out in the open again.

LikeLike